Why Your Boss Buys Your Insurance

A Coverage System Built on Top of Payroll

In the United States, about sixty percent of working-age adults receive their health coverage through their employer. No other rich country relies on its labor market to deliver such a large share of its health-insurance pool. The arrangement is not an inevitable feature of how insurance markets work. It is the product of a specific tax rule and a specific solution to the Rothschild-Stiglitz unraveling problem we studied in Health Insurance 2.

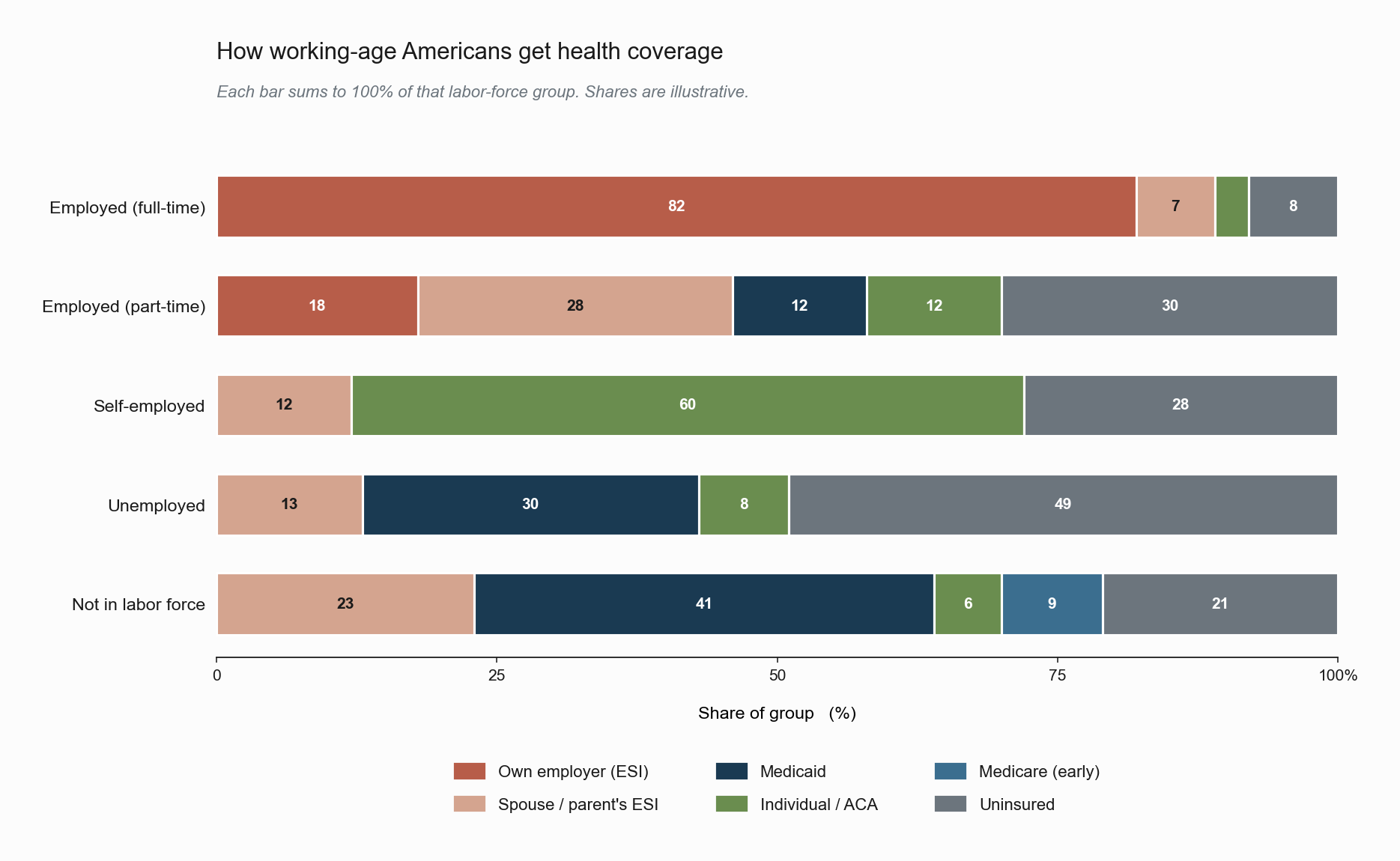

To get a feel for what this looks like at the population level, look at how each labor-force group sources its coverage.

Each row is a labor-force status; the colored segments show the share of that group with each coverage type, summing to 100% within the row. The picture is dominated by a single fact: among full-time workers, roughly 82% are covered through their own employer, and another 7% ride on a spouse’s or parent’s plan. Employer-sponsored insurance (ESI) accounts for nearly nine in ten full-time workers. The other rows tell the rest of the story by negation. As soon as a worker steps off the full-time track, the orange ESI bar collapses. Part-timers fall back on a patchwork of spousal coverage, Medicaid, and the ACA marketplace, with close to a third uninsured. The self-employed lean heavily on the individual market the ACA built, but still leave more than a quarter uncovered. Among the unemployed, Medicaid picks up roughly 30%, while about half remain uninsured. Outside the labor force, Medicaid becomes the dominant source, supplemented by early Medicare for those near retirement. If a different country drew this picture, every row would be a single color, the source of coverage independent of work status. The U.S. picture is shaped almost entirely by the institution we are about to examine.

This note explains why the institution exists, how its tax treatment shapes wages and coverage simultaneously, and why it imposes a mobility cost on workers that has no analogue in any of the canonical insurance models. The mobility cost is the door we walk through into the next series. Everything we built in the labor-economics notes (the outside option \(W_0(x)\), the acceptance set \(\{(x,y) : S(x,y) \ge 0\}\), the firm effect \(\psi_j\) as a composite of three forces) will reappear once we model the lock-in.

Historical Accident, Institutional Lock-In

Employer-sponsored insurance (ESI) is a twentieth-century artifact with two anchors.

The first is a wartime accident. During the Second World War, the U.S. government imposed wage controls on civilian employers to suppress inflation. Firms competing for scarce labor could not raise cash wages, so they began to offer non-wage benefits, chief among them health insurance, as a way to make their offers more attractive. The Internal Revenue Service then ruled, first administratively in 1943 and then by statute in the Internal Revenue Code of 1954, that employer-paid health premiums were excluded from the employee’s taxable income. This tax exclusion is the single most important federal subsidy to health insurance in the United States. The Joint Committee on Taxation estimates its annual cost at roughly two to three hundred billion dollars in forgone revenue.

The second is the Employee Retirement Income Security Act of 1974 (ERISA), which created the legal framework under which large employers could self-insure their workforce. ERISA exempts self-funded employer plans from most state-level insurance regulation, making it administratively feasible for large firms to operate their own risk pools rather than purchase coverage in the individual market. By the time the modern ACA marketplaces were created in 2014, this institutional architecture was already half a century old, and the fraction of the working-age population covered through employers had become the central institutional fact of U.S. health policy.

The path-dependence here is important. There is no economic argument that requires health insurance to be bundled with employment. The institution exists because two policy choices made for unrelated reasons interacted to make the bundle privately attractive, and once the bundle was established, dismantling it is costly because it has been priced into wages, into firm size distributions, and into the structure of competing markets.

The Tax Wedge

The mechanics of the tax exclusion are stark when written down formally. Suppose a worker has marginal income-tax rate \(\tau\), and consider two ways the firm can spend a marginal dollar on this worker’s compensation.

- Cash wages. Every $1 paid as cash wage becomes $\((1 - \tau)\) in the worker’s pocket.

- Employer-paid insurance. Every $1 paid as a health-plan premium becomes $1 of in-kind compensation that the worker would otherwise have to buy in after-tax dollars.

The implicit subsidy to employer-paid coverage is therefore \(\tau / (1 - \tau)\) in proportional terms. A worker facing a 30 percent combined marginal rate of federal income tax, payroll tax, and state income tax receives roughly $1.43 of equivalent value from each dollar of ESI compared to cash. The wedge widens with income because marginal tax rates are progressive, which is why high-wage workers tend to receive disproportionately generous ESI packages.

| Marginal tax rate \(\tau\) | Take-home from $1 cash | Take-home from $1 ESI | Implicit ESI subsidy \(\tau/(1-\tau)\) |

|---|---|---|---|

| 0% | $1.00 | $1.00 | 0% |

| 15% | $0.85 | $1.00 | 18% |

| 25% | $0.75 | $1.00 | 33% |

| 35% | $0.65 | $1.00 | 54% |

| 45% | $0.55 | $1.00 | 82% |

Imagine a worker named Alex in the 35% marginal-rate bracket. His employer is deciding whether to spend an extra $1,000 on his compensation. If the firm pays $1,000 in cash, Alex takes home $650 after tax. If the firm pays $1,000 toward Alex’s health plan instead, Alex receives $1,000 worth of coverage. The pre-tax cost to the firm is the same in both cases. But the after-tax value to Alex is $350 higher if it comes in the form of coverage. Multiply this across the workforce and you get the basic reason high-paying firms tend to offer generous health plans: it is a tax-efficient way to compensate workers, and the higher the worker’s tax bracket, the more efficient it is.

The tax exclusion is, in effect, a regressive subsidy that pays workers more for receiving compensation in kind than in cash, with a larger marginal price wedge for those who face higher marginal tax rates. The fiscal cost is real. The equity profile is one of the most well-known critiques of the institution.

The incidence question, that is, who actually pays for the employer’s premium contribution, is the natural follow-on. Gruber (1994) used variation in state-level mandates that required employers to cover maternity care to estimate the incidence empirically. Wages of workers most affected by the mandate fell by roughly the cost of the mandated benefit, consistent with the textbook prediction that workers value the benefit at close to its cost and therefore bear its incidence in lower wages. This is the compensating-differentials logic we developed in Search and Matching 5, applied to the largest non-wage amenity in the U.S. labor market.

Employer Pooling and the Rothschild-Stiglitz Escape

The tax wedge explains why ESI is generous. It does not by itself explain why ESI exists as a risk-pooling institution at all. The complementary answer is institutional: the employer pool is a way to avoid the unraveling result of Rothschild and Stiglitz.

Recall the R-S problem. In a competitive individual market with private information about risk, the low-risk type is rationed and pooling cannot survive entry. The collapse is driven by the ability of workers to sort themselves into the contract that best matches their type, which is what gives the cream-skimming deviation its bite.

Within a firm, that sorting margin is closed off. The decision to take a job is driven by many things (wage, location, career trajectory), not solely by the value of the firm’s health plan. Conditional on accepting employment, workers are typically enrolled in a default plan or choose from a small menu, and they cannot use plan-specific selection to undermine the pool the way they could in an individual marketplace. The firm therefore effectively acts as a mandatory risk pool, with the additional property that the pool’s composition is determined by who chooses to work at the firm rather than by who chooses to buy each plan.

A concrete illustration: at a typical mid-sized firm of two hundred employees, the pool includes the marathoner and the diabetic from Health Insurance 2 together. Neither of them can switch into or out of the pool just because of their health risk. The marathoner cannot sign up for an individual plan that excludes the diabetic, because she is committed to working at the firm for other reasons. The diabetic cannot cherry-pick the firm just for its health plan, because hiring committees screen on more than insurance demand. The firm has, in effect, bundled enrollment with an unrelated decision (employment), and that bundling is what stabilizes the pool.

This is not nothing. By bundling the insurance contract with a separate decision (the labor contract) on which workers have heterogeneous preferences, the firm pool is partially shielded from the cream-skimming dynamics that destroy the individual market. The size, demographics, and industrial composition of the firm all influence the resulting pool, and firms of different types end up offering different effective premiums to similar workers, which, in turn, becomes a piece of the firm effect \(\psi_j\).

The Bridge to the Labor Series

Let us close this note by stating the connection precisely. Recall from Search and Matching 2 that a worker of type \(x\) accepts a match with a firm of type \(y\) if and only if the surplus is non-negative, \[

S(x, y) \;\ge\; 0,

\] where the surplus depends on the outside option \(W_0(x)\). Job lock changes \(W_0(x)\) in a structured way. For a worker with health risk \(h\), the value of being in the unemployment-search pool is reduced because that pool comes without the firm’s tax-subsidized risk-pooling. The effective outside option becomes \[

W_0(x, h) \;=\; W_0(x) \;-\; w_{\text{lock}}(h),

\] where \(w_{\text{lock}}(h)\) is the lock wedge, increasing in \(h\). The higher the worker’s health risk, the more the absence of portable coverage depresses their willingness to leave their current job.

This single modification to \(W_0\) has consequences throughout the labor model. It deforms the acceptance set, distorts the AKM firm effect \(\psi_j\) in a way we anticipated in Search and Matching 5, and changes how mobility responds to outside offers.

References

Currie, J., & Madrian, B. C. (1999). Health, Health Insurance and the Labor Market. In O. Ashenfelter & D. Card (Eds.), Handbook of Labor Economics (Vol. 3, Part C, pp. 3309–3416). Elsevier.

Gruber, J. (1994). The Incidence of Mandated Maternity Benefits. American Economic Review, 84(3), 622–641.

Gruber, J. (2011). The Tax Exclusion for Employer-Sponsored Health Insurance. National Tax Journal, 64(2, Part 2), 511–530.

Madrian, B. C. (1994). Employment-Based Health Insurance and Job Mobility: Is There Evidence of Job-Lock? Quarterly Journal of Economics, 109(1), 27–54.