Why a Higher-Paying Job Isn’t Always Better

The Rosen Benchmark: Full Offset in a Frictionless World

Let each firm \(j\) be characterized by an amenity bundle \(a_j\) (working conditions, benefits, hours, culture). A worker’s flow utility from being employed at firm \(j\) at wage \(w\) is \[ u(w, a_j) = w + v(a_j), \] where \(v(\cdot)\) converts the amenity bundle into its dollar-equivalent value for the marginal worker. The worker’s effective value of working at firm \(j\) is the total compensation \[ \phi_j \equiv w_j + v(a_j). \]

The intuition behind this equation is something everyone who has ever evaluated a job offer already knows. Your real take-home from a job is what you earn in cash plus the dollar value of the things the job gives you for free. If your job comes with a $15,000 health plan you would otherwise have to buy yourself, you should add that to your salary when comparing offers. The equation just writes that down.

Suppose, as in Becker’s frictionless benchmark from Search and Matching 1, that workers costlessly observe all firms and can switch jobs at no cost. Then in equilibrium, all firms employing the same worker type must offer the same \(\phi\), otherwise the dominated firms could not retain anyone. Holding worker type fixed, this means \[

\phi_j = \bar{\phi} \quad\Longrightarrow\quad w_j = \bar{\phi} - v(a_j).

\] Subtracting the worker-side AKM effect \(\theta_i\) from both sides (which the law of one price absorbs into \(\bar{\phi}\)), the firm wage premium in this world is \[

\psi_j = -\,v(a_j) + \text{constant}.

\]

This is full offset. The wage premium is the negative of the amenity value. A generous-amenity firm pays less in cash, and the empirical regression of \(\psi_j\) on \(v(a_j)\) would have a slope of exactly \(-1\).

Going back to the kitchen-table example, in a perfectly frictionless world the Seattle and Columbus offers should make you exactly indifferent. The $20,000 cash gap is supposed to be exactly the dollar value of everything the Columbus job has and the Seattle job does not. If you compute total compensation and find that one of them clearly dominates, the only thing keeping the equilibrium together is that someone less picky than you would take the dominated one at this wage.

Reading \(\psi_j\) as quality is a category error in the Rosen world. A low-\(\psi\) firm is one whose amenities have already done the heavy lifting. A high-\(\psi\) firm is one whose cash wage is compensating for something the worker would rather not have.

Adding Friction: Hwang-Mortensen-Reed and the Offset Wedge

Suppose firms differ along two dimensions: a productivity component \(y_j\) and an amenity component \(a_j\). The firm’s wage premium can then be written, in reduced form, as \[ \psi_j = \delta\, y_j \;-\; \beta\, v(a_j) \;+\; \varepsilon_j, \] where \(\delta > 0\) is the rent share of productivity passed through to wages and \(\beta \in [0,1]\) is the offset rate on amenities. The two polar cases are familiar:

- \(\beta = 1\): full Rosen offset. The marginal worker is perfectly mobile, and amenity costs are fully passed through to wages.

- \(\beta = 0\): full monopsony. The firm pays nothing for the cost of providing (or not providing) the amenity. Workers absorb the entire amenity burden in utility.

Realistic frictional models, including Burdett-Mortensen with amenities, Hwang-Mortensen-Reed, and Bonhomme-Lamadon-Manresa, generically deliver an interior \(\beta \in (0,1)\).

It helps to put a number to this. Suppose a firm provides a health plan worth $10,000 to the average worker. Under full offset (\(\beta = 1\)), that firm pays $10,000 less in cash than an identical firm without the plan. Under partial offset (\(\beta = 0.5\)), it pays $5,000 less. Under no offset (\(\beta = 0\)), it pays the same as the other firm and the worker collects $10,000 of pure rent in the form of the benefit. Friction is what determines where along this range the market actually sits.

The crucial observation, and the one most often missed in applied work, is that the sign of \(\mathrm{corr}(\psi_j, v(a_j))\) depends on the joint distribution of \((y_j, a_j)\) and on \(\beta\). When productivity and amenities are positively sorted across firms, that is, when good firms tend to be good along both margins, the productivity channel pulls \(\psi\) up where amenities are high while the offset channel pulls \(\psi\) down. Their net is theoretically ambiguous.

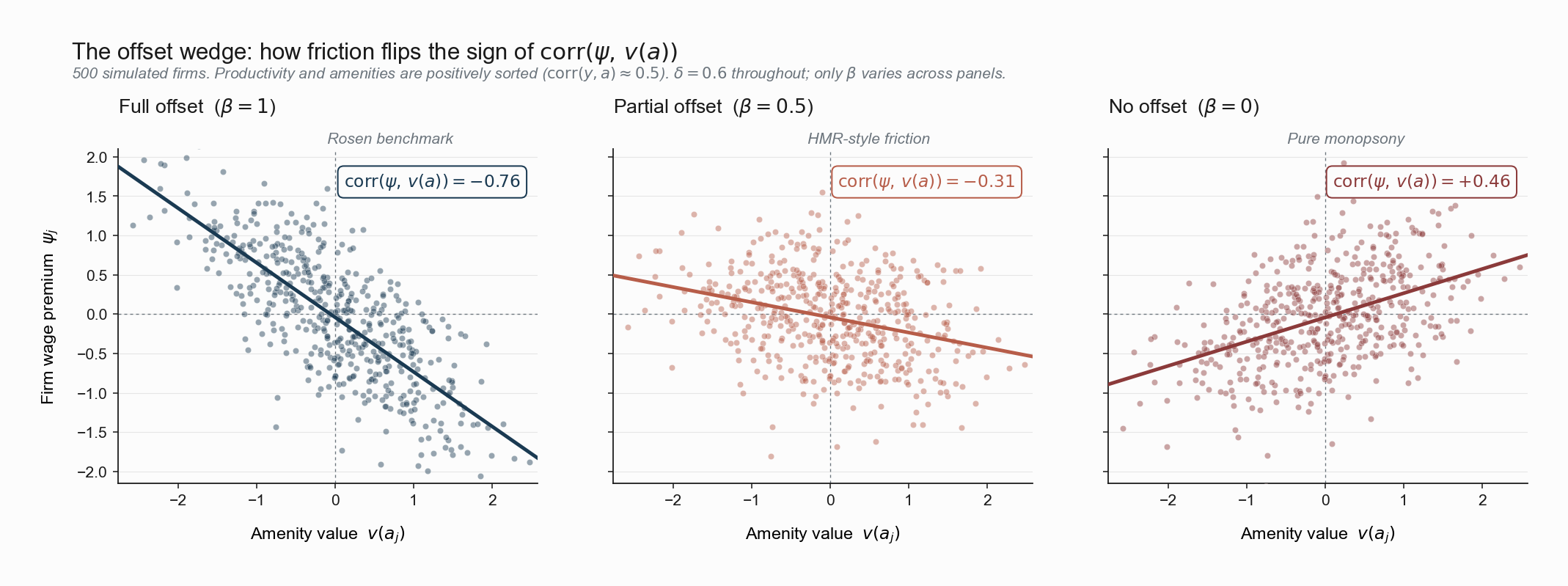

The figure below makes this concrete. We simulate 500 firms with \(\mathrm{corr}(y, a) \approx 0.5\), hold \(\delta\) fixed, and vary the offset rate \(\beta\).

Reproduce the figure

import numpy as np, matplotlib.pyplot as plt

rng = np.random.default_rng(20260522)

N = 500

y = rng.normal(0.0, 1.0, N) # firm productivity (latent)

a = 0.5 * y + rng.normal(0.0, 0.75, N) # amenity, positively sorted with y

eps = rng.normal(0.0, 0.20, N)

delta = 0.6 # productivity rent passthrough

for beta in (1.0, 0.5, 0.0):

psi = delta * y - beta * a + eps

print(beta, np.corrcoef(a, psi)[0, 1])In the leftmost panel (\(\beta=1\), full offset), \(\mathrm{corr}(\psi, v(a)) \approx -0.76\). The Rosen prediction holds: cash wages compensate for bad amenities. The middle panel (\(\beta=0.5\), partial offset under friction) preserves the sign of the relationship but attenuates it to \(-0.31\). The rightmost panel (\(\beta = 0\), extreme monopsony) flips the sign to \(+0.46\), because now only the productivity channel, which is positively correlated with amenities by construction, remains visible.

Two lessons follow.

First, the sign of the observed correlation between \(\psi\) and amenities is a structural diagnostic. A strongly negative correlation is evidence that markets approximate Rosen’s frictionless benchmark. A near-zero or positive correlation is evidence of either substantial monopsony or a strong productivity-amenity sorting (and probably both).

Second, the magnitude of \(\psi_j\) is no longer a clean measure of firm “quality” in any of these worlds. In the full-offset world, low \(\psi\) means good amenities. In the no-offset world, high \(\psi\) comes bundled with good amenities. Reading \(\psi_j\) literally as a firm pay premium misses two thirds of the story.

Sorkin’s Trick: Watch Where People Move, Not What They Get Paid

If wages can be misleading about how good a job is, what can we use instead? In Search and Matching 3 we introduced Sorkin’s (2018) revealed-preference approach as a method for ranking firms. Here, that ranking has a deeper structural meaning.

The key observation is that workers’ mobility decisions, unlike their wages, are driven by total compensation \(\phi_j = \psi_j + v(a_j)\), not by the cash wage \(\psi_j\) alone. If workers systematically leave firm \(j\) for firm \(k\) but not vice versa, then revealed preference says \(\phi_k > \phi_j\), even if \(\psi_k < \psi_j\).

Think of it this way. If everyone you know who works at the Seattle tech firm is quietly applying to the Columbus university, but no one is going the other way, you have an answer about which job is actually better to hold, regardless of which one’s cash wage is higher. Workers vote with their feet, and their feet observe the total package, not just the cash.

This gives a two-equation identification:

- Wage-level data identify \(\psi_j\).

- Poaching-flow data identify \(\phi_j\) (up to scale, via the PageRank-like algorithm in Sorkin’s paper).

The amenity value is then identified residually: \[ v(a_j) \;=\; \phi_j \;-\; \psi_j. \]

Sorkin’s headline finding is that approximately two thirds of the variance of firm value \(\phi_j\) comes from non-wage characteristics, that is, from \(v(a_j)\) rather than from \(\psi_j\). Whatever workers are sorting on, it is mostly not the cash wage. This is a striking number. It says that if you ranked firms by what workers actually choose to work at, and ranked them again by the wage premium they pay, the two rankings would disagree on most of what makes a firm a good place to work.

Lamadon, Mogstad, and Setzler (2022) embed this insight in a structural model of imperfect competition that decomposes firm effects into rent-sharing and amenity components. Taber and Vejlin (2020) push further by combining the revealed-preference logic with Roy-style selection on comparative advantage. Across these papers, the recurrent finding is that amenities are first-order, not residual, and that ignoring them gives misleading welfare conclusions about firm-driven wage inequality.

The Handoff: The Most Policy-Relevant Amenity

The compensating-differentials literature traditionally focuses on amenities that are easy to measure but small in dollar terms: commute time, schedule flexibility, on-site amenities. The single largest non-wage amenity in the American labor market, by an order of magnitude, is employer-sponsored health insurance. For a middle-aged worker with a family, \(v(a_j)\) from health coverage alone can plausibly run into five-digit dollar values per year. The Columbus offer in the kitchen-table example was already mostly about health insurance, even if we did not name it as such.

It is also the amenity for which all three of Rosen’s frictionless conditions fail simultaneously. The tax exclusion of employer premiums creates a fiscal wedge that distorts the relative price of cash and in-kind compensation. The employer pool generates an information rent that the individual insurance market cannot offer. And the non-portability of coverage across employers creates a search friction with no analogue in the standard amenity literature. A worker who leaves a firm loses not just the wage but the pool.

How does the most important amenity in the U.S. labor market distort the wage premium \(\psi_j\), the sorting \(\mathrm{Cov}(\theta_i, \psi_j)\), and the welfare cost of mismatch, all at once? I will discuss these in the next series.

References

Hwang, H., Mortensen, D. T., & Reed, W. R. (1998). Hedonic Wages and Labor Market Search. Journal of Labor Economics, 16(4), 815–847.

Lamadon, T., Mogstad, M., & Setzler, B. (2022). Imperfect Competition, Compensating Differentials, and Rent Sharing in the U.S. Labor Market. American Economic Review, 112(1), 169–212.

Rosen, S. (1986). The Theory of Equalizing Differences. In O. Ashenfelter & R. Layard (Eds.), Handbook of Labor Economics (Vol. 1, pp. 641–692). Elsevier.

Sorkin, I. (2018). Ranking Firms Using Revealed Preference. The Quarterly Journal of Economics, 133(1), 353–401.

Taber, C., & Vejlin, R. (2020). Estimation of a Roy/Search/Compensating Differential Model of the Labor Market. Econometrica, 88(3), 1031–1069.